India Real Estate 2025 Report

India’s residential real estate market is on a trajectory of rapid expansion, forecast to reach USD 540 billion in 2025 and nearly double in the coming decade. For Japanese firms, this sector presents significant opportunities, both in traditional development and in new-age urban solutions, driven by macroeconomic tailwinds, demographic transformation, and rising digitalization.

Indian Market Overview & Dynamics

- Growth Velocity: Indian residential real estate is projected to maintain a double-digit CAGR (approx. 12%), outpacing global averages (~3%) and driven by a burgeoning middle class, urbanization, and growing IT/ITeS workforce.

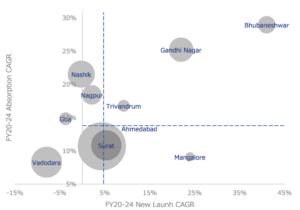

- Top Geographies: Tier I cities (Mumbai, Bengaluru, Hyderabad, NCR) and select Tier II markets (Ahmedabad, Surat, Gandhinagar) exhibit robust absorption and launch rates, with Maharashtra and Gujarat dominating new supply.

- Segment Evolution: Increasing demand for mid-segment and premium housing, high-rise developments in metros, and niche luxury villas in peri-urban and Tier II areas.

Key Drivers for Successful Entry in India

- Regulatory Reforms: Recent initiatives, such as RERA and the SWAMIH Fund, have improved transparency and reduced risks for global investors. Japanese companies can now form direct JVs, participate in co-development, or pursue asset-light partnerships.

- Consumer Trends: Nuclearization of families, NRI demand, and a preference for digitally enabled home buying experiences are creating new product and channel opportunities.

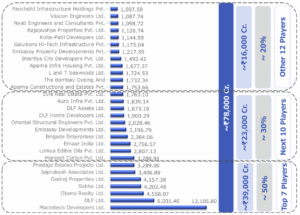

Competitive Landscape dominated by regional players

Thirty developers earn more than ₹1,000 crore annually, yet the sector’s true competitive strength lies in land acquisition and upfront capital.

The largest seven players account for about half the segment’s annual revenue, but regional and local developer strengths are determined by access to high-demand geographies.

Strategic Entry Approaches for a Foreign Real Estate Developer

- Joint Ventures & Strategic Alliances: Collaborate with top local developers (e.g., Lodha, DLF, Prestige, Godrej), combining Japanese capital, technology, and project management standards with local land access and market knowledge.

- Localization and Adaptation: Develop India-specific housing solutions; optimize cost structures; customize amenities and design to local preferences while leveraging Japanese reliability and brand equity.

Risks & Mitigation Tactics to be considered

- Policy Variability: State-level differences in stamp duty, building codes, and tax levies require targeted legal and compliance advisory.

- Land & Capital Barriers: Prime land acquisition is resource-intensive and acquisition of land is subject to FDI prohibitions basis usage type. Entering as co-investors or via phased asset-light models can mitigate upfront risk.

- Exit Options: IPOs and M&A are emerging but require patient capital and well-established local partnerships.

Imperatives for Japanese Companies

Strategic questions for new entrants include:

- Land Ownership: Determining who can own project land, and structuring agreements (purchase, rent, long-term lease, or short-term lease) with Indian landowners.

- Entry Route: Evaluating options such as tying up with established local players or establishing a direct subsidiary in India.

- Compliance: Understanding regulations on profit repatriation, minimum investment amounts, taxation, reporting, and especially the implications of RERA.

- Risk Factors: Addressing slow insolvency resolution for stressed projects (affecting supply), high state-level duties and stamp levies, and rising mortgage rates impacting affordability.

Summary

India’s residential real estate is ripe with opportunities for Japanese corporates. Success demands a nuanced local strategy: robust partnerships, regulatory diligence, and a keen grasp of geographic and segment dynamics. Early movers stand to gain significant market share and long-term value by leveraging India’s urbanization, sectoral reforms, and evolving consumer demand. The next decade will offer not only commercial returns, but also the chance to shape the urban transformation of one of the world’s fastest-growing economies.

Dream Incubator Inc. (DIAI India Private Limited)

For further consulting on entry strategies, partnership models, and risk management, contact Dream Incubator Inc. (DIAI India Private Limited), with offices in Japan and India. Reach Ms. Diana Roy (Director) or Mr. Jay M Jetani (Associate Manager) at WeWork Galaxy, Bengaluru.